How to Convert 401k to Roth IRA Without Paying Taxes is a question many smart retirees and investors ask when planning their financial future. The idea is simple: you want the tax-free growth and withdrawals of a Roth IRA, but you don’t want to hand over a big chunk of your savings to the IRS during the conversion.

In this guide, we’ll explore proven, legal strategies that can help you move money from your 401k to a Roth IRA with little or no tax cost. You’ll learn exactly how the process works, what rules you need to follow, and how to make the most of this powerful retirement planning move.

If you’ve been building your retirement savings through a 401(k) and now you’re thinking about the long-term tax benefits of a Roth IRA, you might be asking the million-dollar question:

“Is there a way to convert my 401k to a Roth IRA without paying taxes?”

The short answer: It’s possible to minimize or delay taxes — but avoiding them entirely requires smart planning, specific timing, and using IRS-approved strategies.

In this guide, I’ll walk you through the process, the rules you need to know, and legal strategies that can help you reduce or eliminate taxes when making the switch.

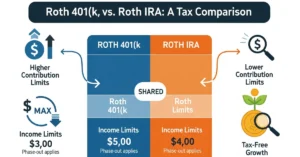

Why Convert a 401k to a Roth IRA?

Before we talk about avoiding taxes, let’s quickly cover why people make the conversion in the first place.

A Roth IRA offers:

- Tax-Free Withdrawals in Retirement – Once you hit age 59½ and meet the 5-year rule, your withdrawals are 100% tax-free.

- No Required Minimum Distributions (RMDs) – Unlike a 401k or Traditional IRA, you won’t be forced to withdraw money at a certain age.

- Better Estate Planning Benefits – Your heirs can inherit the account with fewer tax headaches.

- More Investment Flexibility – Roth IRAs typically offer more investment choices than an employer’s 401k plan.

If you expect to be in a higher tax bracket in retirement, converting now can save you thousands in future taxes.

The Tax Problem with Converting

Here’s the challenge:

- Money in your 401k is pre-tax — you haven’t paid income taxes on it yet.

- When you move it to a Roth IRA, the IRS treats it as a taxable distribution for that year.

- This means you’ll owe income taxes on the amount converted.

Example:

If you convert $100,000 from your 401k to a Roth IRA and you’re in the 24% tax bracket, you could owe $24,000 in taxes.

So the goal is to find ways to legally reduce or avoid that tax hit.

7 Strategies to Convert 401k to Roth IRA Without Paying Taxes

Below are proven strategies people use to minimize or eliminate taxes during the conversion.

1. Convert in a Low-Income Year

Taxes are based on your income for the year. If you can plan your conversion during a year when your income is unusually low, you may pay little or no taxes.

Examples of low-income years:

- The year after you retire but before you start Social Security

- A year when you take a career break or work part-time

- A year with significant business losses or deductions

Tip: If your taxable income falls below certain thresholds, you could pay 0% on the conversion.

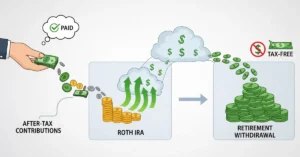

2. Use After-Tax Contributions in Your 401k

Some employers allow after-tax contributions to your 401k (different from Roth 401k contributions).

You can roll over just the after-tax portion to a Roth IRA — and since you already paid taxes on that money, there’s no tax due on conversion.

This strategy is often called the “Mega Backdoor Roth”.

3. Roll to a Traditional IRA First, Then Convert Gradually

Instead of converting your entire 401k at once, you can:

- Roll it into a Traditional IRA (no taxes on this step).

- Convert small portions to a Roth IRA over several years.

By spreading conversions, you keep each year’s income lower — reducing your overall tax rate.

4. Offset with Tax Deductions

If you have large tax deductions in the same year you convert, you can wipe out the tax bill.

Common big deductions:

- Business expenses (if self-employed)

- Real estate depreciation

- Charitable donations

- Medical expenses (above the AGI threshold)

Example:

If you convert $50,000 but have $50,000 in deductions, your taxable income from the conversion could be $0.

5. Use a Health Savings Account (HSA) to Cover Taxes

While this doesn’t remove the taxes from the conversion, it can make it painless.

If you have an HSA with a big balance, you can withdraw tax-free for medical expenses — freeing up cash to pay your Roth conversion taxes without touching your investments.

6. Move to a State with No Income Tax Before Conversion

If you live in a high-tax state like California or New York, you could face state income taxes on top of federal taxes during the conversion.

By moving to a state with 0% income tax (like Florida, Texas, or Nevada) before converting, you can save thousands.

7. Leverage the Standard Deduction & Lower Tax Brackets

Everyone gets a standard deduction ($14,600 for singles in 2024, $29,200 for married couples). If your conversion amount fits under your standard deduction + lower tax brackets, you can pay little to nothing in taxes.

Step-by-Step: How to Convert 401k to Roth IRA

Here’s a simple roadmap:

- Check with Your Employer Plan – Ask if they allow an in-service rollover (if you’re still working) or plan a rollover after leaving your job.

- Decide Direct or Indirect Rollover – A direct rollover (custodian-to-custodian) avoids penalties and is simpler.

- Open a Roth IRA – If you don’t have one, open it with your preferred broker.

- Plan the Conversion Amount – Use strategies above to reduce taxes.

- Complete the Transfer – Your 401k provider will move funds directly to the Roth IRA.

- Set Aside Money for Taxes – If you owe taxes, don’t use retirement funds to pay them — use separate savings.

Common Mistakes to Avoid

- Converting Too Much at Once – This can push you into a high tax bracket.

- Not Understanding the 5-Year Rule – Each Roth conversion has its own 5-year clock before tax-free withdrawals.

- Doing an Indirect Rollover Without Care – If you miss the 60-day deadline, the IRS treats it as a withdrawal (taxes + penalties).

Final Thoughts: How to Convert 401k to Roth IRA Without Paying Taxes

Converting a 401k to a Roth IRA can be one of the smartest retirement moves you make — but it requires strategic planning to avoid or minimize taxes.

The bottom line:

- Use low-income years, deductions, and after-tax contributions to your advantage.

- Spread conversions over time instead of doing it all at once.

- Consider your state’s tax laws before pulling the trigger.

By following these steps, you can build a tax-free income stream for retirement while keeping more of your hard-earned money.

FAQ

Can I really avoid paying taxes entirely on a 401k to Roth IRA conversion?

Yes, but only if your taxable income is low enough to stay in the 0% bracket, or if you’re converting after-tax 401k contributions.

Is it worth paying taxes now to get a Roth IRA?

If you expect higher taxes in retirement, yes. You’ll trade a smaller tax bill now for tax-free withdrawals later.

What’s the best age to convert?

Many people convert in their early retirement years (ages 60–65) before RMDs start.

Will I be penalized for converting my 401k to a Roth IRA?

No, there’s no early withdrawal penalty if the funds go directly from your 401k to a Roth IRA. However, you may owe income taxes unless you follow tax-minimizing strategies.

Can I convert my 401k to a Roth IRA while still employed?

Yes, if your employer allows an in-service rollover. Not all plans permit this, so check with your HR or plan administrator.